Put your money where your model is.

Duty to the Public

Your honest credence is a distribution: everything you believe in your heart of hearts about the values the future might realize, and how plausible each is, given your model, assumptions, and data at the time. When the job demands a single number—as it usually does—your loss function dictates the statistic: the mean under squared error, or the median under absolute loss. Here we'll assume squared error, hence the mean. Whatever the summary, it comes from the same distribution: the one you'd bet on.

From the American Academy of Actuaries Code of Professional Conduct (emphasis mine):

"Precept 1. An Actuary shall act honestly, with integrity and competence, and in a manner to fulfill the profession's responsibility to the public and to uphold the reputation of the actuarial profession.

Annotation 1-1. An Actuary shall perform Actuarial Services with skill and care.

Annotation 1-4. An Actuary shall not engage in any professional conduct involving dishonesty, fraud, deceit, or misrepresentation or commit any act that reflects adversely on the actuarial profession."

These commands seem obvious, but wait and see.

First, and I it hope goes without saying, the actuary believes the phenomenon they're forecasting can be modeled in a way that puts probability mass towards the yet realized outcome—that modeling is a worthwhile exercise, that it will help the actuary to play to win.

Second, let's agree that the actuary should always consider all relevant material data when forecasting. They do not arbitrarily ignore some of the data. In other words, the actuary is completely non-ideological. Otherwise they risk selection and confirmation bias. (I'm borrowing from E. T. Jaynes here.)

Last, let's assume you're working with distributions like an actuary who remembers Exam P (Remember, the "P" stands for probability, or have you spent too many hours in Excel with only point-estimates!). You're forecasting; nothing is certain, so the distribution encodes all the future values that might be realized and how plausible you think they are now. You have a distribution, and the expected value is a statistic of that distribution.

Stray Paths

Again, to meet these commands, the actuary should report, for each quantity, their honest credence—or the expected value of their distribution when using one number. Not the number you prefer. Not the one your principal prefers. Not the number that simplifies your life and keeps stakeholders off your back. Consider these three failure modes:

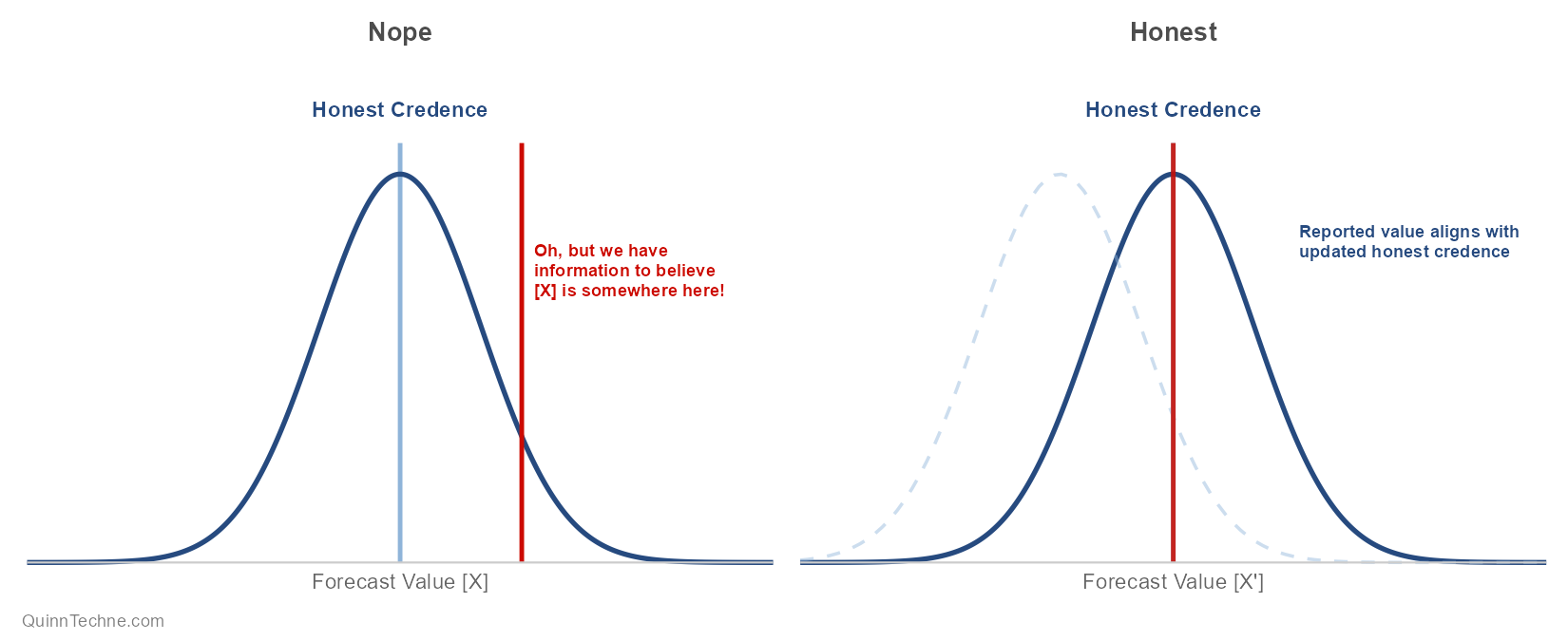

1: The Unquantified Override

"Oh, well, we modeled [X], but we're going with [Y] because we know [Z]." No! If [Z] is material, your credence must condition on it, which means quantifying its effect, not gesturing at it. Update the model and use the new [X'] mean. "We know [Z]" is the start of an update, not a substitute for one. And you don't get to ignore [Z] either—you're a non-ideological actuary, remember?

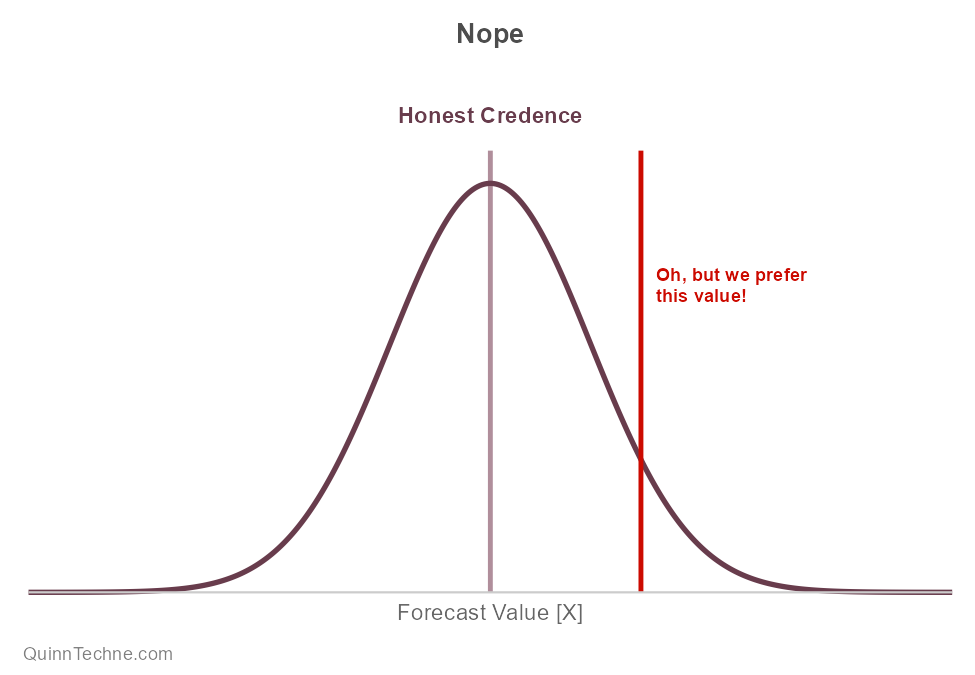

2: Conservatism in the Wrong Spot

"Oh, well, we modeled [X], but we're worried about solvency, so we added [Y] conservatism." No! You're forecasting. Forecasting is prediction, not a preference. Conservatism is a preference. Conservatism, margin, provision for adverse deviation—it's not yours to add to the prediction. Why? Because you have a principal. They have preferences. And they can make decisions by combining their preferences with your predictions. Honesty preserves the principal's autonomy. Predict first, then disclose any margin separately. (There may be cases where you are both the actuary and principal. If so, congratulations—do whatever you want.)

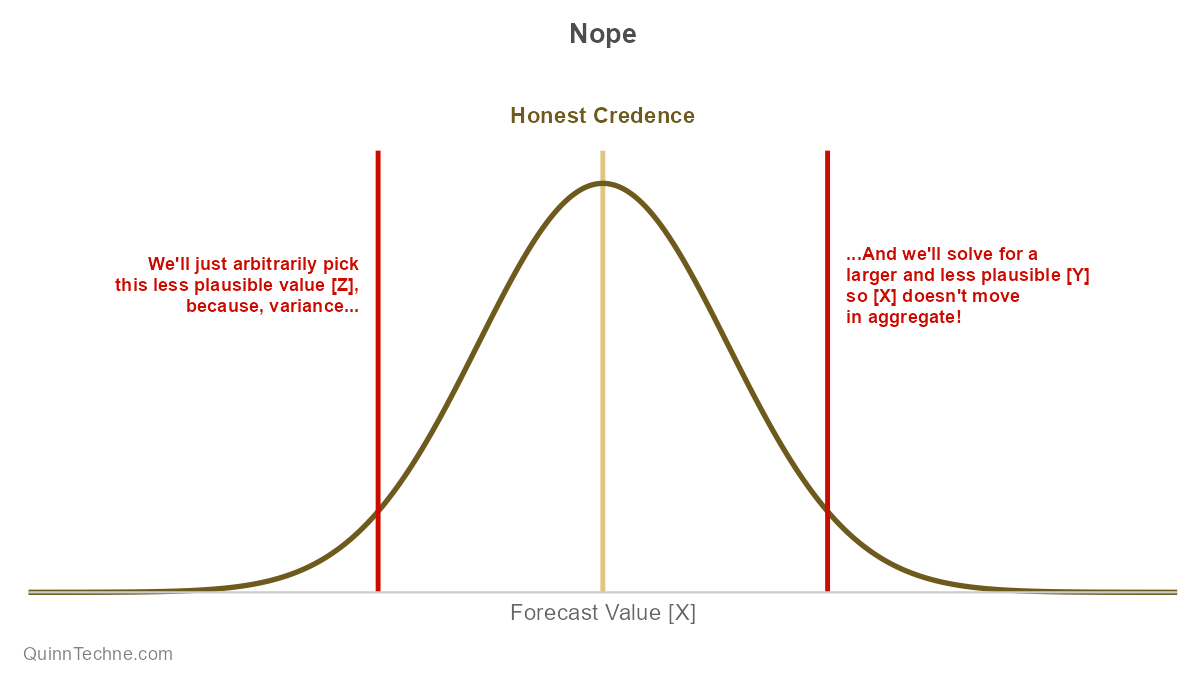

3: Two Wrongs Don't Make an Average

Subcomponent E[Y] + E[Z] = E[X]. "Oh, well, we modeled [X], but we want to say assumption [Y] is bigger than our honest credence because it makes our stakeholders ask fewer questions, so we chose to report a less plausible value of [Z] and offset it by a bigger [Y] so in aggregate [X] is the same value, and because [X] didn't change, we're fine." No! This decision misleads readers who assume you are reporting your most honest number, because nothing suggests otherwise. Don't report values of [Z] and [Y] that sit away from their expected values. Suppose the actuary is accidentally doing this, varying assumptions away from their expected values, instead of using an aggregate distribution that already accounts for all combinations and their frequencies. In this case, the actuary is uninformed and not doing this part of their work with skill and care.

Creed

Actuaries are frequently forecasting. Forecast to win. Encode everything you know into your priors, and consider all the data when you update to the posterior. Report the honest expected value of your forecast. Conservatism, margin, provision for adverse deviation are all fine, but they belong to the principal: bosses, clients, regulators and their prescribed standards. Margin may even be required by law. And that's fine: prediction first, then preference. Document the prediction and disclose the margin separately, because readers will take your number as your honest estimate unless you tell them otherwise Don't usurp the principal's autonomy by biasing your forecast. Give only your honest credence.

American Academy of Actuaries. (2001, January 1). Code of Professional Conduct. https://www.actuary.org/sites/default/files/files/code_of_conduct.8_1.pdf

Harris, S. (2011). Lying. Four Elephants Press. https://www.samharris.org/books/lying

Jaynes, E. T. (2003). Probability Theory: The Logic of Science. Cambridge University Press. http://www.med.mcgill.ca/epidemiology/hanley/bios601/GaussianModel/JaynesProbabilityTheory.pdf

Calculations and graphics done in R version 4.3.3, with these packages:

Pedersen T (2024). patchwork: The Composer of Plots. R package version 1.2.0. https://CRAN.R-project.org/package=patchwork

Wickham H, et al. (2019). Welcome to the tidyverse. Journal of Open Source Software, 4 (43), 1686. https://doi.org/10.21105/joss.01686

The views and opinions expressed in this article are those of the author and do not represent the official policy or position of any employer, organization, or entity. This article is for informational and educational purposes only and does not constitute professional actuarial advice.

Generative AIs like Anthropic's Claude Fable 5 were used in parts of the writing review and coding. The author did the Suminagashi cover.

{kind=link}